The Week Ahead: Kevin Time!

--Warsh Begins --

--Warsh Batman Begins --

Round and round the strait of Hormuz

Kevin Warsh chased a rate cut

Iran refused to cut a deal

‘POP’ goes the rate cut

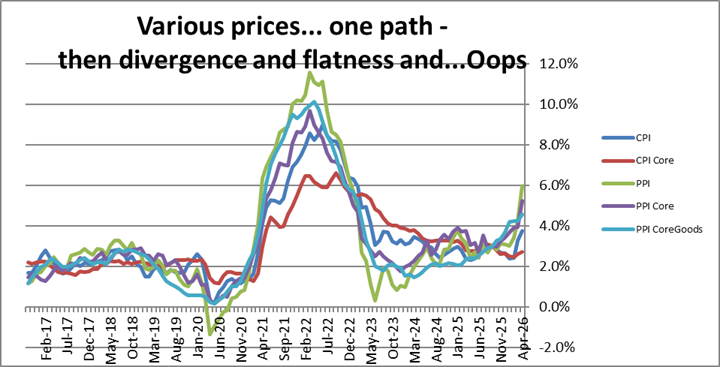

Up, Up, and Away: A Not-So-Beautiful Inflation Balloon: CPI

PPI-FD shows spike clean through to the core and services

Note that post-spike the level of inflation was still higher than its pre-spike pace.

A penny for a spool of thread

A dollar for a needle

Too-expensive to go out to eat

POP goes the rate cut

Powell Bequeaths a monetary mess to Warsh, and stays on to watch the fun

Monetary policy offers a parallax view. <<Parallax view refers to the apparent shift in position of an object when observed from different viewpoints. >> especially for those with a political perspective. If you view Warsh as a Trumpy and Powell as anti-Trumpy none of this will make sense to you because you already have staked out a specific perspective. And from behind your ‘pillar of truth,’ you will not be able to see reality since your view is obstructed. Tough nuggies. Time to detach and explore for truth…and think.

Warsh has a long history at the Fed and from being at Treasury and commenting independently on markets. He resigned from his position of governor at the Fed and offered his own Op-Ed explanation that he opposed the ongoing QE, which he viewed as excessive.

So how surprised could anyone be that he has come back to the Fed with a view that the balance sheet is ‘too large’? All the QE run for a period of about 18 years has put a lot of fat on the Fed balance sheet. At least that is how Kevin sees it. Some see it as a balance sheet built to support the banking system. But the banking system was also built to need a large balance sheet, so that point is hardly fair.

Whatever your view, it is worthwhile to consider arguments on the other side. Some look at the balance sheet and the banking system’s operations and argue that it works; leave it alone. Others say the balance sheet is as small as it can be. On the other side, they look at the legacy of inflation—over target for 5 years and running. And they look at mortgages on the balance sheet—clearly evidence of the Fed mucking around in fiscal policy—non-monetary business—and they say no more!

The way to get the Fed focused on hitting its prescribed targets and staying out of fiscal policy is to give it a balance sheet that is less likely to be misused—keep it small. A large balance sheet is simply there asking to be misused. And politicians always have ideas and the ‘best of intentions.’

Bill Dudley has been one of those who assert that the balance sheet can’t be reduced. And specialists agree with him—at least accepting the way the balance sheet is currently being used and under current Fed operating techniques and given current banking regulations. But changes in these elements could permit the balance sheet to be smaller. So, Warsh is about broader change, not just naively changing the balance sheet.

When Warsh was first selected for this job, he was talking about productivity, making inflation lower, and making a lower Fed funds rate possible. However, higher productivity raises R-star, the estimate of the equilibrium Fed funds rate, since growth is stronger with stronger productivity. With productivity gains still looking solid and with inflation rising—even for services—the prospect for a rate cut looks more remote and less feasible—not more feasible.

Most of the people we have talked to recently have said that JOB-ONE for Mr. Warsh would be controlling inflation and him getting established as a trusted leader at the Fed—building the right bridges to collegiality.

Some of Warsh‘s early remarks may have been misinterpreted since some think he intends to come in and muzzle Fed communications. However,

he seems to really prefer to have a more open discussion at FOMC meetings where the rubber meets the road to get a consensus on policy and then to have the FOMC close ranks on that policy.

It is a different approach from Mr. Powell’s having all these pre-FOMC-meeting one-on-ones and getting the agreements he seeks for the policy he wants. After that experience, FOMC members want to go public and express their true views. Remember, the FOMC statements are expressed on a policy course that voters either endorse or COULD ACCEPT—the latter a much looser criterion. So, it’s not surprising members who may have been cajoled to accept a policy course may have wanted to give a speech highlighting what they were not able to say in the FOMC vote.

Warsh’s idea seems to be instead to make everyone’s idea count at the meeting. Do not herd people to a conclusion. Let the committee vote. Make that policy. Then close ranks around the single decision. One criticism of the previous policy is that it confused markets, with different viewpoints being expressed in public. Warsh wants to eliminate or reduce that effect.

Out-of-control inflation

Inflation is out of control. Fed (Powell) defenders will blame it on tariffs or the war and spiking oil prices. And, of course, there is something to those arguments, but, as always, not enough. Inflation is really ‘MADE’ by bad monetary policy. Let’s not forget the early 1970s brought an end to the fixed exchange rate system and the gold standard. In 1968 OPEC was formed, and in the early 1970s it flexed its muscle, and then the Arab oil embargo kicked in during the 1973-75 recession as inflation shot higher. So, the point is that monetary policy faces many temptations. And when it succumbs to the temptation, monetary policy is at fault, not the temptation itself. Monetary policy has many arguments to swerve from its goal of stable prices. But choosing to swerve is a monetary policy decision. To swerve to foster more growth, to lower the unemployment rate, to swerve to elect certain partisans, to soften the relative price jump for oil, and so on. These are all monetary policy decisions. All of them are wrong, made for the wrong reason. But all of these are simply temptations, and many of them are really bogus arguments. Anything that takes the Fed away from its number-one goal of price stability is a mistake. Stability is the key that unlocks the way to better growth and lowers unemployment over time. Fiscal policy is in the realm of Congress, not the Fed. By giving the Fed a goal of full employment, Congress has assigned to the Fed a goal that it has no tools to achieve; that goal needs fiscal policy.

Central bank tactics

Volcker and Greenspan

But a dual mandate sounds good. Yet, it does—and has—greatly complicated Fed policymaking. Controlling inflation is what it can do. The dual mandate is a creature of Congress; the Fed simply has to develop a plan to deal with it. Volcker and Greenspan had a plan. It was to target the long-term Phillips curve, not the short-run Phillips curve. The Fed made policy for the long run focused on price stability, and Volcker and Greenspan had great success getting inflation down and keeping it down.

Bernanke

Bernanke’s inflation targeting was a bait-and-switch policy that never made sense in practice. He had a dual mandate! Bernanke embraced it and yet sold us on the idea of the Fed pursuing an inflation-focused agenda. That was never the reality of it—the real agenda was a shared policy goal. Through Bernanke’s term, the conflict was never apparent. But after Covid the conflict emerged, and under Jay Powell the Fed flipped the switch and prioritized the unemployment mandate. Bernanke’s promised land of price stability disappeared. That was never Bernanke’s plan. But Bernanke enabled it to happen, and even as a past Fed chair, he watched Powell in action ruin what Bernanke had sold to us as policy. And yet, Bernanke never was critical of Powell.

So, enter Kevin Warsh…

No wonder Warsh is a shock wave. He also is a shock because Trump wants him to do the undoable. After five years of inflation overshooting, tariffs still in play, and oil prices through the roof, Trump STILL wants rate cuts. I hear people arguing now that Warsh will cut rates. Well, I hope not. It’s the worst thing a Fed chair could do under these circumstances. Warsh will be hard-pressed to not hike rates—in fact, he may hike rates!

What Powell did

Before you go all soft and mushy on Powell and how difficult it was to be under constant pressure from Trump, remember his overshooting on inflation was persistent and was his choice. Five years over target – and counting. Blaming it on war, tariffs, and oil prices is simply not sensible and not for a five-year stretch—one that began with inflation denial so the Fed could hold rates and he could get renominated.

Why the central bank should get back to target quickly

One reason you want the central bank to get back to target quickly is because the future is uncertain. Another reason is to give the message that, yes, 2% is the target, not 2.5%, not 2.8%. When the Fed takes the view Powell did that, it had presided over a long period of price stability so it could allow prices to drift slowly back down to target, which ignored the FACT that the modern economy is often buffeted by shocks, and when a shock comes, you would like the flexibility to act. But if you get an inflation temptation like tariffs or high oil prices and you already have been over target for 4 or 5 years, you are in trouble. Now inflation is going to rise from an already elevated position. And that is very bad.

I am not arguing that Powell should have known Trump would impose tariffs or that oil prices would spurt. But those shocks happen, and they are unpredictable. When the Fed gives its SEPs four times a year, it does it from the current reality, projecting ahead to two to two-and-a-half years ahead on the notion that the forecast period will be smooth sailing. That assumption is a mistake, and it is another reason why the Fed should push for policy to get back to 2% inflation before the end of its forecast period, so it has policy slack and flexibility in the period ahead.

Powell did not do that and instead simply tried to ride on the Fed’s past achievements. In a recent ECB speech, Christine Lagarde argued that the central bank was always trying to build credibility. Her view was that the central banks never had credibility to consume. But Mr. Powell consumed credibility for five years, running and asserting inflation expectations remained anchored, and the Fed engaged in a disastrous run of over-target inflation.

The future is now

Monetary policy is now going to be made differently. We can argue about what that means. In truth, none of us really knows. I prefer to look at Kevin Warsh’s background. At the Hoover conference we attended a week ago in Palo Alto, Marvin Barth offered a paper in which he used a designation of Hawk/Dove that has been worked up to analyze Kevin Warsh’s policy stance when he was a Fed governor. Bath demonstrates how it was used to show that Warsh was hawkish during Democrats holding sway at the White House and dovish when Republicans held sway. Barth does not dispute the result, but he then demonstrates how wrong that analysis is by showing that this hawk/dove measure actually is much better correlated with a series on GDP growth. Warsh was making policy decisions—regardless of the White House occupant—relative to economic performance, as one should.

So, there is a lot of analysis out there. Not all of it is ‘good’ or ‘fair’ or ‘accurate.’ Be sure to know the drink maker before sipping or guzzling the Kool-Aid.

Inflation is rising. Much of it is because of oil. But it is also deeply ingrained in services and inherited from past trends. Mr. Warsh will have his work cut out for him. He will not want to antagonize Trump. But he must make good and necessary policy decisions. He needs to demonstrate his leadership to the FOMC, proving that they can trust him. He has a number of hats he has to wear, and policymaking is a process. He is important, but he does not control it. It is going to be difficult. So, prejudge him at your own risk.

Calendar

END