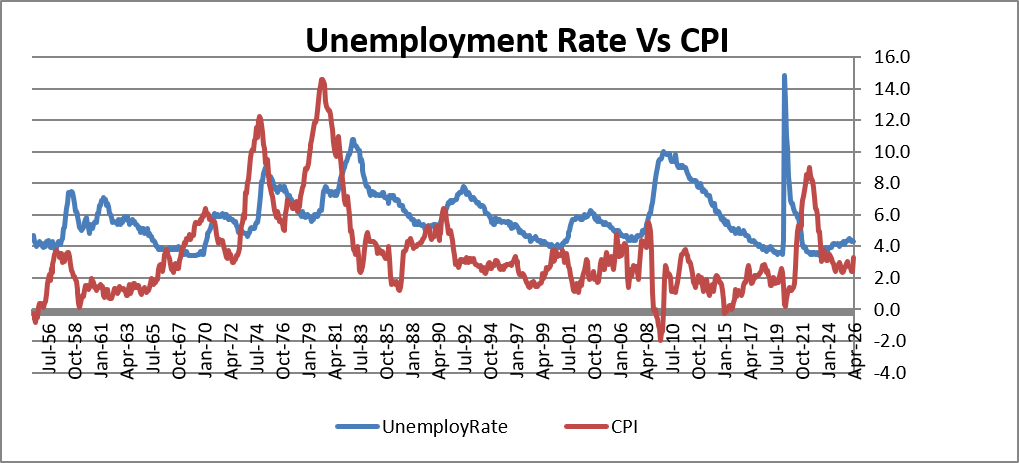

The Week Ahead

A new day is dawning- does that mean a new night, too?

A new day is dawning- does that mean a new night, too?

One year trend: shortest

Trends are where you draw them.

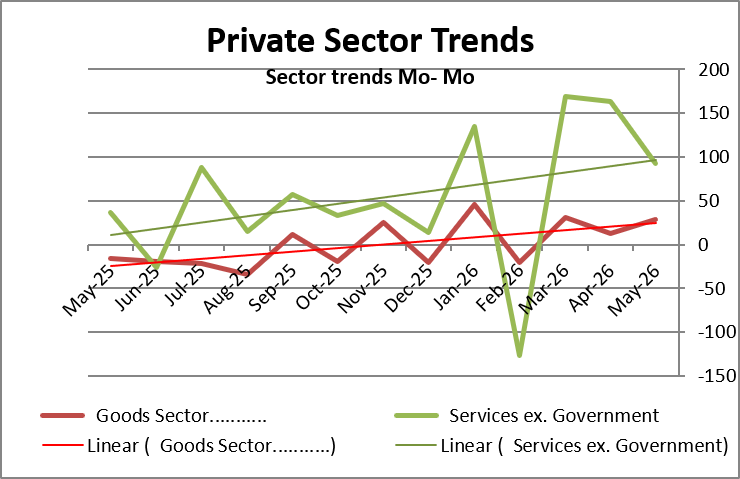

Two years

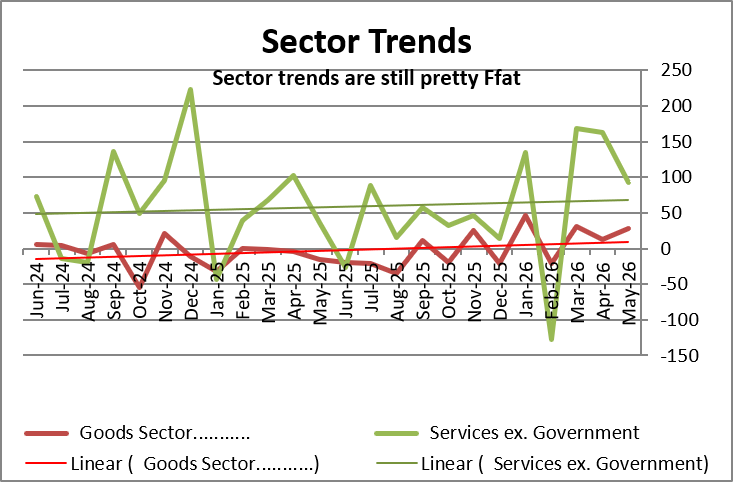

Since 2024: flat

Three-year trend

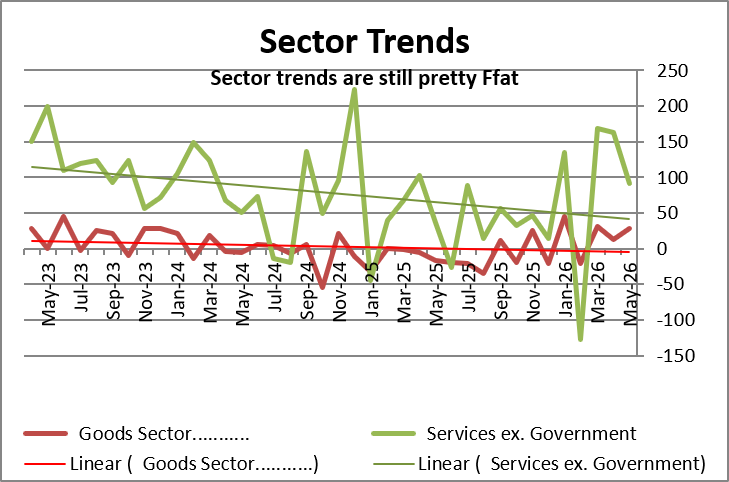

Since 2023 – lower

Mathematical trends are calculated according to a computational design. I’m speaking here of a trend line calculated from data, rather than eyeballing some kind of time series and imposing a judgmental trend line on it. The trends above are calculated using mathematical principles, not by eyeballing the data. The calculations show that over three years the trend for job growth points lower; over 2 years the trend is relatively flat; however, over the last year the trends are pointing up. So you can get the result you want from the trend depending on the period that you choose to calculate it. However, I think the trends also have meaning. Over the past year there’s been a lot of concern about job growth and weakness in the economy, particularly in the labor market. What we’re seeing in the last few months is evidence that that weakness was transitory and possibly related to the government shutdowns that lingered.

The end of resilience and the start of trouble?

To be sure, the economy has been through a lot of turbulence, and there have been a lot of policies, shocks and disruptions that could have untracked growth although it appears that nothing has harmed the economy. It is looking quite firm with the labor market looking solid and has been in over a year Even so Job growth broke higher; we know that the borders are still closed, and we know that the demographics of labor force growth based on domestic statistics is weak. However, one irony is in this situation: there’s a lot of concern about the notion that artificial intelligence (AI) could cost us a lot of jobs. But at this time when labor force growth is weak, maybe having jobs resupplied to the labor market in an intra-marginal way - that is, in terms of making existing labor force participants with skill and experience available to be hired anew—maybe that will help to invigorate the economy rather than to weaken it? The jury is still out on this idea.

POLICY

With this very solid and stronger-than-expected job report, it would have been possible for President Donald Trump to try to declare victory based on his “Big Beautiful Bill” and to back off his past mantra that was pushing for interest rate reductions. However, Mr. Trump did not take that High Road. Mr. Trump is staying on the Low Road of saying he would still like to see interest rates fall and this is going to make things very difficult for the new Fed chairman. Few economists think that the right thing to do when the economy is speeding up and performing well is to cut interest rates. In fact, a further problem this economy has is that although the president claims he is upset by Jerome Powell for not cutting interest rates faster, the inflation rate in the past five years has been continuously over the top of its target. We are not coming out of a period when we would say the Fed has been too-tight. Monetary policy seems to have been consistently too loose. Monetary policy officials have consistently misjudged the economy, expecting it to create lower inflation. And at the same time, there have been persistent shocks of various kinds that have contributed to making inflation higher. However, monetary policy has to work in that environment and has to set a policy that can deal with shocks as they occur to control their effect.

The Fed has not done this and it’s pretty hard to keep up a five-year string of claiming that ‘the dog keeps eating your homework.’ And so here we are again with the new Fed chair coming in, while we know the president wants to cut interest rates. On the day that new chair Kevin Warsh was sworn in, the president urged him to be independent; however, at the end of that little pep talk, he also said that he would very much like to have lower interest rates. We have no question about where the president stands on the question of where interest rates should be.

On the other hand, we have every question about what the Fed chairman will do. He is between a rock and a hard place.

A question of bias…

The issue is broader than the policy that Mr. Warsh will endorse or support because the Fed chair has only one vote on monetary policy among a committee of 12 members. FOMC members have been voting on policy continuously, and things do not ‘shift’ just because there is a new chair. Members have been quite outspoken on their desires for policy; the committee is split. And there are quite a number of members who are concerned about the level of interest rates and the current easing bias that policy has maintained and still professes. Many no longer want that bias and want instead to at least shift the bias to a neutral statement and possibly look to raising rates sometime soon.

Former Fed chair Powell left new chair Warsh with a very divided committee and one that was starting to move toward the idea that the bias in policy would be removed but hadn’t quite gotten to that majority yet. Did the May job report put them over that line? Ironically, Mr. Warsh was proposed and nominated. sworn in by a president who wants lower interest rates and yet is coming into the grasp of a committee that’s decided that it’s time to get rid of the easing bias and possibly to start raising rates. This is clearly going to be a difficult moment. Kevin Warsh.

More than a committee

And in addition to the arithmetic on the committee, there’s also the shift in the economy and what the data are calling for. Four to six months ago when the president was more actively talking about who would be the new Fed chair, circumstances surrounding the economy and its performance looked quite different. Job growth was weaker, and the inflation rate hadn’t really turned up although at that time there were some concerns about the president’s own tariffs. Now there may still be some lingering tariff effects coming through the pipeline, but there clearly are oil price effects from the reduced oil flow through the Strait of Hormuz. In addition to other supply lines globally that have been interrupted by the war in the Middle East.

Kevin Warsh is not unknown in the world of monetary policy. He was a Fed governor before, and he had a voting record. He is probably personally not well known to many members of the committee; he is certainly not known to any of them as their Fed chair. Now, he needs to establish his presence on the committee to get respect from committee members at the start of his term of office. Committee members need to find him reasonable. But at this moment it’s impossible to believe that this transition is going to be compatible with the new chair coming in seeking to cut interest rates, as many think he does…does he?

What the world needs now is…

Not only does the economy not seem to need interest rate cuts, but with the economic strength that’s showing through, it would appear that the current level of rates is not even as restrictive as the Fed has been telling us that it was. There may now be a reason for monetary policy to put more restrictive rates into the system, possibly because of the increase in productivity, which, while it can help keep inflation under control, will also boost growth and be consistent with the higher equilibrium fed funds rate than before. But where does that fit?

Headache No 47?

All of this makes me wonder if the Fed chairman is eligible to engage in advertising promotions. At one point Excedrin had a series of ads where people would do things that gave them headaches and they would take Excedrin for it and their ads would label Excedrin headache 101 or Excedrin headache 102. I think that Mr Warsh is about to have a substantial Excedrin headache.

John Cochran, a professor at Stanford University also with that position at the Hoover Institute, has been a colleague of Kevin Warsh for a number of years. “When we were out there earlier this year,” John said. “I know Kevin Warsh, and no one’s going to tell Kevin Warsh what to do.” As reassuring as that statement is, what is… What is Kevin Warsh going to do?

Existing Committee, new chair, new data, new trend- same president

In his new venture there are a number of constituencies Kevin Warch has to impress. He has to get the respect and control of the Federal Open Market Committee; he certainly doesn’t want to alienate the president at his first FOMC meeting; of course, he needs to reassure the bond market, the financial markets, as well as the foreign exchange market, about the kind of policy that he’s going to endorse. But with the economy beginning to look like it’s more robust than it was earlier on what does that mean? What should Mr. Warsh do in this situation to curry the most favor with the most important of his various constituents?

He has been appointed and so he no longer needs to curry the favor of the president. Recent Supreme Court decisions have made it clear that the president has only limited powers to remove a Federal Reserve chairman, and those will require that he find malfeasance. So, the various clashes that the Fed had with President Trump has resulted in the Federal Reserve actually becoming more insulated and more independent than it was before since the Supreme Court has settled an issue that previously was unsettled, and it was settled to the benefit of the Fed.

Avoid a bad start.

However, Mr. Warsh clearly does not want to start out his new term antagonizing the president. Nor does he want to upset the bond market; the financial markets once you’ve done something to upset them are hard to win back. Typically, policy has to go fairly far in the other direction in order to reassure markets about what they had previously been concerned about after a misstep. Conducting a policy that financial markets will find appropriate is essential. And the Fed chair needs to gain control of his committee and needs to get his committee’s respect. For now, that committee is somewhat mixed, although after this employment report it’s very possible that the committee is going to tilt toward wanting to remove the easing bias that exists in the current policy statement.

Is removing the policy bias enough…too much?

Removing the policy bias might be the easiest thing that Warsh could do that would please some of these interests without unduly antagonizing others. Of course, that would depend upon exactly how it was done and on the language used. The Fed could move the policy statement from a biased statement to a neutral statement, which would imply that rates were just as likely to go up as down in the period ahead. That is not the same thing as saying that the Fed’s getting ready to raise rates, but such a switch would be a precursor to a rate hike move. Announcing a tightening bias would be a more aggressive signal that would run the risk of incurring the wrath of the president—especially because the Fed usually does not go from one bias to the other; it usually goes to neutral in between.

A move into a balanced statement could simply make arguments that policy next could move in either direction or could draw out the scenarios under which each thing might occur, making it clear that rate cuts are still possible even as the Fed admitted that rate hikes might be possible. And that might be enough of a move to quell any rebellion within the FOMC and to keep financial markets on the straight and narrow path. And it might also be a move that could avoid the wrath of Donald Trump, who might still be expected to say after the Fed’s announcement that he continues to expect the Fed will cut interest rates.

The president wants interest rates cut currently not simply because the economy needs them (it does not) but because he wants to reduce the interest cost of the debt which is going to go up if the Fed were to lift rates particularly with the Treasury issuing short term securities to fund new needs.

Make no mistake about it, if the war in the Middle East doesn’t end soon, the impact on oil prices is going to spread more across the economy, and the Federal Reserve is probably going to have to react to that. And if that happens, the president isn’t going to be happy regardless of who the Fed chair is. The president is not always a reasonable person about what he wants. He knows what he wants and he generally thinks that he can get what he wants by putting more pressure on. However, for monetary policy that approach doesn’t work. We will be finding out in the coming months if Mr Trump has figured that out and if he realizes that getting in a feud with the Fed chairman is not going to serve him well… nor will it serve the Fed well. If the president is not able to figure this out, there could be some very dark days ahead. It is my hope that Kevin Warsh and his past relationship to Treasury Secretary Scott Bessent will create a pathway of dialogue that would help to placate the president about those sorts of things that monetary policy has to do given the reality of the times. Having that communications path could be crucial; if it’s not able to work, chances are the next 2 1/2 years could be quite difficult and dark.

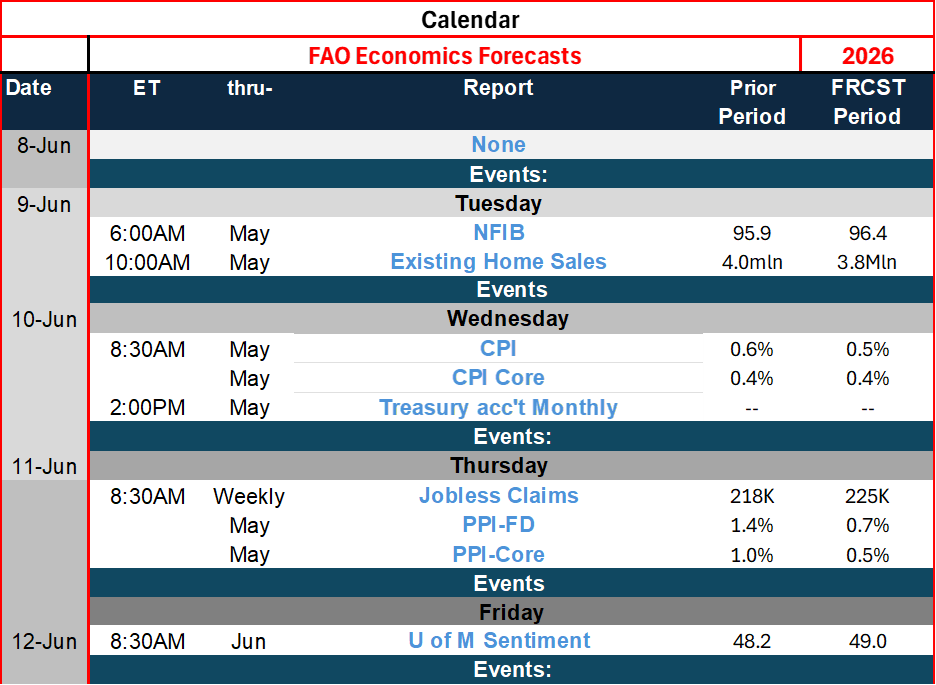

Calendar

END