The Week Ahead And Beyond

Warsh Takes the Oath of Office as FOMC Members Hem Him In...Is the FOMC’s pot calling Kevin Warsh’s kettle black?

Warsh Takes the Oath of Office as FOMC Members Hem Him In

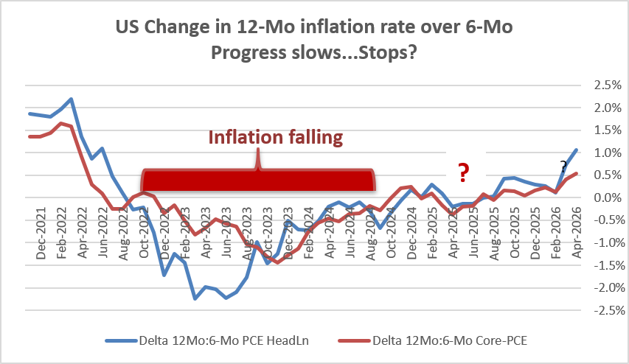

Inflation has been rising and Fed has kept cutting rates!

Is the FOMC’s pot calling Kevin Warsh’s kettle black?

As Kevin Warsh takes his place as chairman of the Fed, we usher in one of the more striking breaks in the administration of monetary policy that we have seen since 1960. Ther appears to be push back against Warsh and his new ideas from a Fed that has failed to hit its target for the last five years. Why do THEY have a superiority complex? Perhaps it is because there is a certain mythology about the US and its understanding of monetary policy and possibly an idea that policy in the US is so on top of the way things ought to be done that the rest of the world emulates what is done in the US. But I think that is mythology and for the most part, wrong. US monetary policy has not been run in a more successful way than it has been run in other countries. US monetary policy has not even frequently been in the vanguard of some of the newer and more important ways to conduct and implement monetary policy. The US was a latecomer to inflation targeting, and when it adopted inflation targeting, it got it all wrong, as you can see.

But the US is the most important country in the world from the standpoint of monetary policy! The dollar is the world’s principal reserve unit, and so the monetary policy made in the US is more important than monetary policy that’s made elsewhere. However, in evaluating US monetary policy and its effectiveness, let’s remember, particularly when looking at what was done under COVID, that the policies run in the US are often followed and mimicked by other countries, so the mistakes that the US made became replicated in other countries along with the fallout from the mistakes that were introduced by those policies. Inflation during Covid was as much led astray by the US as it was global.

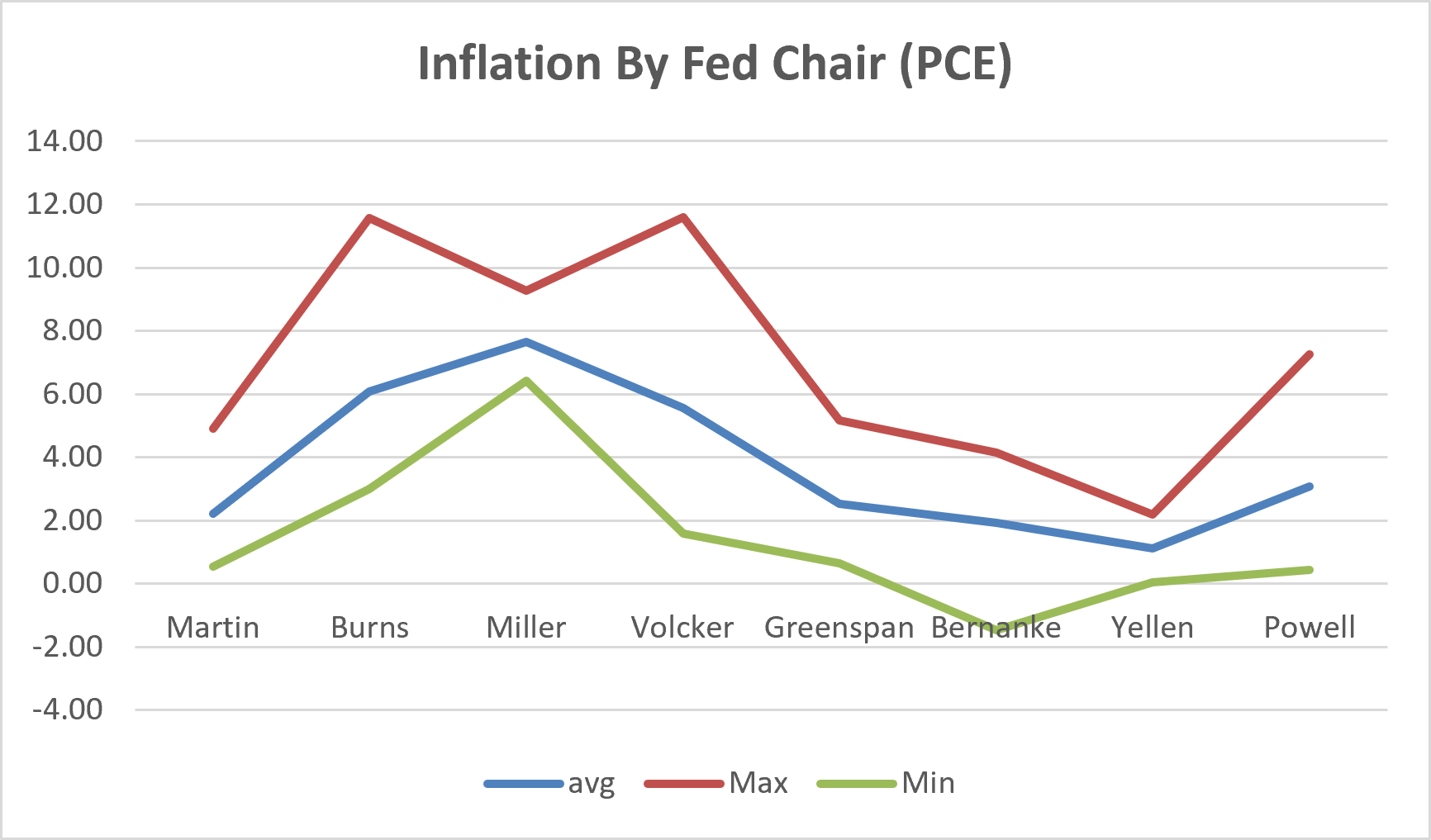

Martin’s data are only from 1960 onward. Powell’s ends in April of 2025

These data basically show us when inflation moved up in the US historically and how it was handled by various Fed chairs. The data are not suitable for ranking the performance of Fed chairs, however. For example Paul Volcker has the highest inflation rate during his term and that’s because he inherited it. The drop-off in the inflation rate from Volcker’s turn to Greenspan’s term is the measure of the success that Volcker had in addressing the inflation problem that he inherited.

If you look at the chart on the real fed funds rate you see the administrations that kept the Fed funds rate above the inflation rate to try to reduce inflation and to control it versus those administrations that didn’t. And, of course, the ones that didn’t are the newest terms under Bernanke, under Yellen, and under Powell. But after the great financial crisis (GFC) a new problem had cropped up and Bernanke did not think that he was trying to fight or reduce inflation; he thought he was fighting the battle of the zero bound and trying to make sure that the Federal Reserve was able to stimulate the economy and keep from getting into a no win situation where inflation turned negative and the Federal Reserve lost its ability to gain traction to stimulate the economy. Because of that concern the Bernanke Fed pioneered techniques to try to impact monetary policy at a time when it had lost its principal vehicle to generate stimulus: cutting the Fed funds rate because of the zero bound.

We can argue about how to evaluate the terms of various Fed chairs. Clearly some of them were in office during periods of more stress and with greater demands than others. Some of them were up to the challenge, and others were not.

Independence and policy

However, during this time the viewpoint began to grow more seriously that the Federal Reserve had to be independent to make good policy and unfortunately one aspect of that was that the Fed to remain in good standing. It wanted to be respected for the policy that it made and in the Fed’s world that apparently meant that The Fed should not be criticized or admit to making mistakes.

Having said this, I don’t know anyone at the Fed who would admit that this is what they think; however, this is definitely the way they act, and people who are critics of the Fed tend to be viewed as almost enemies of the Fed. However, a great supporter of the Federal Reserve and its intellectual work, as well as being a former district bank president, Charles Plosser, in his writings, used to say that Fed independence was extremely important, 9 but that it also was important to criticize the Fed. But the Fed has not been good at absorbing criticism that’s often lashed out at its critics or worse has simply denied that it ever did anything that was very wrong. That is no way to learn and grow.

As the Fed seeks this independence that it believes is so important, it is pretty much without any oversight. Congress is supposed to do the oversight, and there are supposed to be two testimonies each year, each done in two parts, one before the House Financial Services Committee and one before the Senate Banking Committee. However, in 2026 we are moving into June, and the Fed has not had its usual early-in-the-year oversight meeting with Congress. Typically, the Fed would have its first meeting around February and the second one around July. But we’re heading into June and the Fed has not had its first oversight meeting yet. Why? Is the Fed remiss? Is Congress remiss?

And it’s a bit of a stretch to call these oversight meetings. I would expect that an oversight meeting of the Fed would be something that would be conducted by monetary experts in a very serious way rather than by a public testimony by the Fed chair, who would prepare some remarks about the economy and a report about what policy did and then allow his political overseers a Q&A. In this ‘format’ the committee members each get to have about 5 minutes to ask him questions. This is not the kind of oversight that is going to go anywhere or that is going to be productive. Real oversight is not public. And it asks hard questions.

However, there’s a problem here… how to have oversight for the Fed that doesn’t intrude on its independence? This is not an insurmountable problem, and I’m not going to go into any details on how it could be addressed, but it has been a fly-in-the-ointment as far as creating oversight for the Fed and preserving Fed independence. Instead, we’re going to understand the Fed as an entity that is guarding its independence with great jealousy. It is striking out against anything that it perceives to be trying to encroach on that independence, and that has become another part of the problem.

This has been a problem since the Fed has also perceived to have engaged in mission creep, getting involved in things that aren’t clearly part of monetary policy. And this is the aspect of monetary policy that new Fed chair Kevin Walsh wants to take on and rectify.

One problem with the Fed is has become clearer since Gary Stern wrote his watershed book on monetary policy that was not well appreciated at the time called “Too Big to Fail.” There’s been more attention paid to regulation and increasingly what is being done on the regulatory front is impinging on the conduct of monetary policy.

In fact the regulators have required large banks to be able to resolve themselves financially in a crisis by having tremendous access to liquidity. And this is one of the direct factors responsible for the growth in the Federal Reserve balance sheet because banks have a demand for reserves that is incredibly high given their need to cement liquidity and their desire to have liquidity that earns a rate of return. Kevin Warsh’s desire is to scale back the size of the Fed’s balance sheet. That desire is going to have to confront directly this regulatory policy the Fed adopted on banks needs to be able to resolve themselves which has created a huge demand for liquidity and required a large Fed balance sheet.

Many people at the Fed simply defend what the Fed has done and they defend the status quo. A former Federal Reserve Bank of New York president, Bill Dudley, has simply said that the balance sheet can’t be reduced and in making a statement like that I presume what Bill means is that given the current regulations, the demand for reserves that banks have means that the balance sheet is about as small as it can be. Darrell Duffy, an expert on these things at Stanford, essentially holds the same opinion right now except Darrell has written a paper that cites 4 different things that could be done to reduce the size of the Fed’s balance sheet, if it were decided that reducing the size of the Fed’s balance sheet would be a good thing to do.

So far the arguments on balance sheet size, the pros and cons, on haven’t gone very far. The school of thought represented by Kevin Warsh, and I think also well represented by Treasury Secretary Bessent, desires a smaller balance sheet for the purpose of making sure that the Fed sticks to monetary policy and doesn’t have this this massive financial apparatus to manage that could be used for all sorts of things that are not monetary policy. However, engineering a path away from this large balance sheet is going to take some doing and some thinking and some time.

Warsh’s views and perceptions of his views

This brings us to some of the statements that have been made by Kevin Moorish about what he plans to do or would like to do during his term at the Fed. Fed Chairman don’t always come in with a particular agenda; they come in with responsibility to run good monetary policy. However Arthur F Burns took over the Fed and then in the early 70s various economic shocks ranging from the formation of OPEC, OPEC’s decision to exercising market power and raise oil prices sharply, an Arab oil embargo, the US exiting the gold standard and the Bretton Woods system, plunging the world into a fluctuating exchange rate system… these were shocks, these were changes, these were challenges, that Burns simply wasn’t up to handling. And not only blame the Chairman but blame monetary policy that was still learning. At that time the US thought that softening the blow of oil prices by increasing the inflation rate would be a good thing meanwhile in Europe- at a time before the euro had been constructed - the Bundesbank and Germany took a decidedly different view and fought hard to push inflation back down into not accommodate inflation and wound up having a much more successful result with its monetary policy than the Fed.

However, we find ourselves now with another oil price shock of some sort and the lesson of the 1970s which I take to be not to let oil-based inflation take hold, doesn’t seem to be learned ,since many want to treat this oil price shock as if it’s temporary and the expression for this is to ‘see through’ it to the other side and not react to the ramping up of oil prices and instead expect them to ramp back down and to aim policy - not even at an average - but at the ex-post level that you think is going to prevail for oil prices. Perhaps only an economist could have the hubris to think that they know what that is. And this is from a group of people who have a terrible forecasting record but yet they think they know how to do this. So as Warch steps in this is the committee he confronts, and it is not on the same page that he left open when he first expressed his policy views.

Economics has come to depend more on expectations but just forming an expectation for the future doesn’t mean that that expectation will come true. And the central bank that allows the inflation rate to linger over its targets too high and for too long runs the risk that the markets expectations will be altered by this reality and it will lose control of the market as the market will come to see the inflation rate that prevails in the market as the relevant one rather than the one that the central bank claims that it targets. This is particularly important now since the Federal Reserve has for five years been missing its target and yet the Fed continues to assert that inflation expectations are well contained and that it continues to have its credibility as targeting 2% inflation. I really don’t know how an institution like the Fed could be involved in complete and abject failure of reaching its target for half a decade and still think it’s respected. But this is the way the central bank operates in the US and it says things like this pronounced from its central banking pulpit that carries weight and presumably has an impact at least on part of the population. However, there’s another part of the population that doesn’t drink this Kool-Aid and that instead looks at what the Fed is doing and wonders why it’s doing things like this and what it thinks it’s going to achieve?.

Volcker had a special mandate

Central banking in the US has made any number of failures. Paul Volcker came into office as Fed chairman as one of the few chairmen who had a very specific charge: the inflation rate clearly was high, it was too high, it was accelerating, and he came in with a mission to get inflation back under control. There wasn’t an inflation target, there wasn’t a specific objective, just the general objective that things had gotten out of hand and he had to fix things. So he had a mandate, an implicit mandate from the President to do what needed to be done to control inflation. Volcker took those steps raising the Fed funds rate and also stepping a bit out of his own character to admonish Congress for its deficit stoking behavior telling it that interest rates could be lower if Congress would contain its spending. This is something that remains controversial and some people at the Fed think the Fed should not say anything about fiscal policy since the Fed’s job is monetary policy. And, also, because the Fed that wants to be the king of monetary policy doesn’t want Congress telling it how to run its monetary policy.

How doss monetary policy work?

However what has been increasingly clear is that well we have many different monetary theories and while there are things that we can do, some of them only crudely control inflation, the cause of inflation is not well understood and increasingly economists are coming to believe and, I think, to agree that fiscal policy is important for the conduct of monetary policy. But that field is not yet crystallized, and it is not accepted in the mainstream approach of how to run monetary policy.

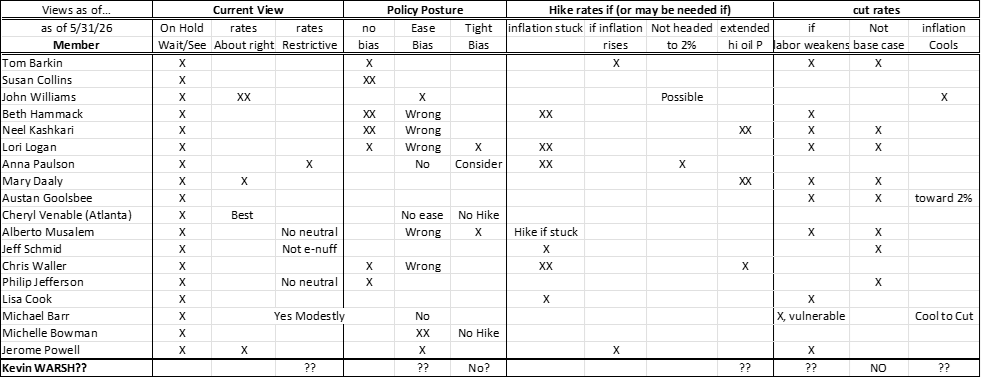

However, at this point of this paper I include a survey which I had AI construct (apologies for that) to arrange and corral the views of FOMC members.

Learning from Bernanke…

And in his run up to being selected, appointed, confirmed, and sworn into office, Kevin Walsh made a number of statements about the Federal Reserve and what his plans are. Federal Reserve Chairmen are often grilled during their confirmation hearings about their philosophies about what they intend to do and Warsh underwent that baptism of fire. Ben Bernanke before him had gone through that as well. At the time there was concern that Bernanke wanted to move to inflation targeting something that a number of congressional members did not want. Bernanke managed to distance himself from that to some extent, however, he eventually went back to trying to get Congress to approve some form of inflation targeting. Unfortunately, the agreement that he got from Congress was to a form of ‘targeting’ that was quite different from the promises that he made to us and to the public about the benefits that we would get from inflation targeting. Bernanke managed a version of inflation targeting that actually breathed new life and to the dual mandate, which brought the Fed’s responsibility to achieve price stability and full employment/maximum job growth- a situation that was in fact, untenable. And in the guise of giving us ‘inflation targeting,’ Bernanke instead gave us a system with two targets and one tool which is a recipe for disaster, which is what ultimately ensued.

Bernanke did not have any particular trouble with the dual mandate during his term. That said he largely undershot the inflation goal during his term. Inflation remained very low on the Janet Yellen’s term as well. But then eventually the framework agreement that had been adopted by Bernanke to run policy was changed and changed for the worse as monetary policy began to go badly off track as the Fed decided it did not have to fight inflation, and did this at the very time that inflation began to appear and accelerate.

The dual mandate creates a forked-tongue at the Fed

We can argue about this perhaps forever. The Fed does have a dual mandate that expresses a mandate to achieve 2% PCE target and to achieve maximum sustainable growth/maximum employment growth whatever that is. That definition has been fuzzed over and changed several ways to make the labor part of the forecast more important than the inflation part less important. At least that was the result under the Powell Fed. That of course is/was an unmitigated mistake, and it led to this disaster that we have in monetary policy.

We already have Congress running fiscal policy to try to create better growth and better working conditions for people. The administration has a Labor Department to attend to issues of Labor in particular. There are also other labor-supporting entities such as National Labor Relations Board (NLRB). But… only the Federal Reserve is responsible for inflation and price level issues.

So when growth or maximum job growth is put on the Fed’s plate along with achieving its inflation objective, the job market mandate is a side dish; the inflation objective is the main course. Make them equal, and you’ll have put two things on the plate that are incompatible. Under Volcker and Greenspan, this problem had been mitigated because they essentially viewed the job growth mandate as a long term mandate and the inflation mandate as a more immediate mandate. The two mandates were and different time horizons. Bernanke and his zeal to have an inflation target agreed to have the inflation objective and the labor market objective put on the same timeline, which created an unresolvable conflict for a central bank with only one tool, the Fed funds rate.

If actions speak louder than words, what has the Fed been telling us?

And after that, what eventually happened is even more bizarre… that is that two term Fed chair Jerome Powell decided that he was going to pursue a soft landing, which meant that he was going to further subordinate the price objective to coddling the unemployment rate. In doing this, he flipped the Fed’s usual priorities by putting the labor market first and the inflation objective second, and this is how we got to a situation where we are five years without having seen the Fed hit its 2% inflation target. And yet the Fed tells us it has credibility, and it tells us that inflation expectations are still anchored. For my part I can’t imagine what logically would lead anybody to draw those conclusions from those facts.

Back to basics

So Kevin Warsh has a number of objectives that he has set forth to try to undo some of the things that have been done ...many of them by the current sitting FOMC. These range from adjusting the overly large balance sheet of the Fed, to doing things in the guise of monetary policy that are not monetary policy and to renewing the Fed’s focus on a 2% inflation objective. Although when Warsh was first in some sense, running for this job he also mentioned that he thought interest rates could continue to fall and he cited artificial intelligence gains and ongoing gains in productivity as things that might be able to lead the Fed to further rate reductions even though we’re still five years without hitting the inflation target. Does Kevin still believe that as a near term tactic? I do not know.

A dynamic world

However, it’s a dynamic world, and things change. And from the time that Kevin Walsh began talking about these objectives there has been a full-blown war in the Middle East; the Strait of Hormuz has been shuttered; oil prices have jumped dramatically; inflation is on the rise. Frankly, it’s hard for me to think that Kevin Warsh still is of the opinion that he can cut rates anytime soon. Now, of course, I don’t know what he’s thinking and what he’s planning and to what extent he may still think that AI is doing marvelous things with core inflation despite what’s going on with energy inflation. But it’s also true that other FOMC members have been hearing this and they’ve been having their own view of what’s going on and expressing what they want to happen.

Monetary stew has many ingredients and chefs

Monetary policy is not made by the dictate of the chairman it’s made by a vote of a committee and the chairman is only one of 12 votes on the committee that votes to set interest rates. One thing that Kevin Walsh had mentioned is that he thought there were too many Fed officials talking and he thought it was confusing from the standpoint of communicating policy. This has caused some district bank presidents and others to think that the new chairman intends to try to muzzle the public statements of the FOMC.

But… it’s true that Federal Reserve officials speak often, and they have different points of view and I think it can be confusing to try to figure out exactly what policy is. The table above in this paper shows where various FOMC members - not all of them voters—stand. It is confusing.

What Warsh has really said (what he probably means)

However, if anyone has really listened to all the remarks that Kevin Warsh has made, then you know he has said is that he is looking to create a much more open environment for discussing and arguing about monetary policy at the FOMC meetings. Once policy is decided in a much more open forum I believe what he means is that he would then like to see the committee come together behind that policy publicly and to endorse it rather than to see various members speak out as individuals indicating their separate personal preferences.

Free debate or pre-arranged debate?

If monetary policy debate is behind the closed doors of the FOMC that really is the engine of making monetary policy, and if that discussion is made open to everyone, I don’t see how that could be an inferior situation to the way Fed has been running policy in recent years. In fact, it seems to be a direct step up from the way Jerome Powell has done things since we know that it has been Powell’s tendency to meet with people individually before meetings to try to create the consensus he’s going to want at the meetings. Those individual meetings undercut the value of committee discussions and also rob the country of the frank exchange of views we are supposed to get in the delayed release of the FOMC transcripts.

Bear witness to the truth.

What we have been witnessing recently are a number of FOMC members saying things in public that I think have the effect of pushing Kevin Warsh into a corner. A number of members, knowing that Warch has been on the record about cutting interest rates (eventually) are quite explicit about not wanting to do that (now) and about not wanting a rate cut bias on the books. And some are about wanting to make sure that rate hikes around the table. Of course all of this lives in a world of perception because you really don’t know given all the changes that have occurred in the global economy where Mr. Walsh stands on the issue of rate cuts versus rate hikes. We know on the day of his being sworn in both he and the president talked about the importance of Federal Reserve independence. Many people don’t think that President Trump meant that and that that it was a remark for show but I think that we’re about to find out. I also think this FOMC that has brought us 5-years of inflation overshooting and has until very recently been voting to cut rates with inflation over its target- need to get a grip on reality as well as on history and on their role in making it what it has been.

Warsh has been an anti-inflation FOMC member

And Kevin Warch’s previous stay on the FOMC (he had been a governor previously) his voting record shows him to have been one who made hawkish decisions when the economy required hawkish decisions and dovish decisions when the economy required dovish was decisions. Eventually he resigned from the FOMC when he saw quantitative easing (QE) or if you prefer large scale asset purchases (LSAP) as being conducted on a scale that he thought was inappropriate. And now of course we have this large balance sheet which he thinks is inappropriate and that he would like to pare back.

Has the Fed become more political than collegial?

The Fed is supposed to be collegial, and we know the Chairman doesn’t come in and simply tell FOMC members what he wants them to do. Not only does the new chair have to be respectful of the members, but the members need to be respectful of the new chair. And it strikes me that the FOMC members in this instance have done a lot more throwing down the gauntlet to Kevin Warsh than they have been trying to help him bring the committee to some kind of consensus.

Powell FOMC, which Jerome Powell has been engineering and pushing into rate cuts rather persistently even with excess inflation has developed a blowback to Mr. Powell’s position, and there have been recent significant dissents on the committee, and we are aware that there is a divided committee about whether the current policy bias should stay or whether it should go to neutral. A number of FOMC members have held forth in public their opinions which has the effect of putting people with the other opinion on the defensive and among the people that that might affect would be the new chairman. Why not save all this talk for the FOMC meeting? Why do it in public?

Could this talk have been tempered?

My question is if there wasn’t a way that many of these people could have talked about the situation as more of a challenge rather than as a situation in which they had a strong opinion? Kevin Warsh has done everything he could in public to tell people that he wants there to be free and open discussions at FOMC meetings (he has referred to it as potentially family feud) about what people want policy to be. Why isn’t that enough? Why have FOMC members been unwilling to simply wait to express themselves behind closed doors where they can have their knock down drag out fights with other members of the committee and possibly with the chairman to decide what monetary policy is going to be? Why has it been so important for them to stake out these public opinions, which will then either be reflected or not reflected in the conduct of policy when the next FOMC decision is made? How is any of that conduct superior to keeping it all behind closed doors…from the standpoint of making good monetary policy? I simply don’t see it.

Warsh as proxy-Trump

Instead, what I see is an FOMC that is getting a chairman who they think reflects the views of a president with whom the FOMC has been at odds and whom they wants to make sure knows who’s boss and that is that they are the majority and he is the chair-minority. And while we don’t hear this kind of rhetoric from the committee per se I think it’s pretty hard to look at the actions of the committee, the thing is they’re saying in public, and to reconcile it with the idea that they are going to give Kevin Warsh a fair hearing on his views whatever they may be…

Ah Kevin we hardly knew ye

At this point I can only say I don’t know what his views will be or are. The situation on the global economy has been ever-changing, and there are a number of different approaches that could be used to conduct policy. However, the Fed has been missing its targets for the last five years, and let’s remember what that means it means that the members of this committee are responsible for having conducted policy and acted to implement the policy that has been wrong for the last five years. In other words, this isn’t exactly the committee that ought to be standing on any moral high ground and telling a new chairman that they know better what to do. These are the people who followed the leadership of Jerome Powell down the road to perdition and to five years of inflation overshooting. And now they appear to be wary about taking advice from a new chairman. Really?

Still…not Mr Perfect

I would be much happier if Mr. Warsh, coming into this position, was saying first and foremost and he is going to be dedicated to making sure that the Fed hits its inflation target of 2% rather than continuing to string it out the way it was done in the past. I am not a fan of the Fed cutting interest rates and telling me that its models or its forecasts tell us that cutting interest rates is going to be fine because inflation is going to be falling in the future even though they’re cutting interest rates today. And I will have that skepticism even if you tell me they’re very sure that AI is going to be able to deliver the goods (the lower goods prices!). And that’s partly because I’ve used AI and I’m very skeptical of what it can do and very careful about using it because I know that it makes mistakes.

A new day dawning…but with the same weather?

I am looking forward to a new Fed chair. The Fed desperately needed change and has needed to shift policy. Jerome Powell was clearly leading the Fed in the wrong direction for too long and, while he may have had control of the committee, he had lost the sense of what monetary policy was supposed to be and what it was supposed to do. One of the great ironies of chair Powell is that he allowed inflation to overshoot for so long and that he strung out this long period of rate reductions at a time that president Trump wanted interest rates to be even lower and - despite Powell having cut of interest rates again and again with inflation over the top of its target- acting, you would seem to think, very much in line with the way the President would have wanted, the President and Jerome Powell continued to be at great odds with one another.

Power to the People! Not to the Fed

I think the answer to this is that it wasn’t really over policy at least not over his unwillingness to cut interest rates faster or deeper but rather because of Mr. Powell’s dabbling in politics particularly the rate cuts that he helped to engineer ahead of the 2024 elections that made no sense and that infuriated Trump, potentially helping Harris. Also, whatever else anybody wants to say, spending $3 ½ billion dollars on renovations to the Fed without getting any approval for this was really a huge mistake of Powell’s. People who are accusing the President of being off base for being critical of Mr. Powell for doing this, I think, are on shaky ground. People argue that this wasn’t monetary policy! So, why is the president getting involved? One answer is since this wasn’t monetary policy, then it clearly is fiscal spending and therefore it’s fiscal policy, and it’s the Federal Reserve impounding funds that otherwise would have gone to treasury and that would have been available to the American public and since it’s not monetary policy, the President was fully within his rights to be critical of the Fed chair interdicting these funds to spend them on staff emoluments. And to ask him what he thought he was doing seems reasonable. Does the Fed chair Powell think that anything that a Federal Reserve official does is monetary policy and therefore can’t be criticized because the Fed should be independent? Well, I don’t think the Fed independence gives anybody on the Fed that kind of a bubble of protection, do you? So once again, we are back on the doorstep of this idea of Fed independence that is so murkily defined and once again getting the Fed in trouble. The Fed did not want to seek permission to spend the money because then it would be acknowledging that someone held power over it. The Fed really needs to get a clear delineation of what its power is and what it is not.

Conflict and friction

And this is one of the key issues: The Fed needs to be independent in matters related to monetary policy, and there needs to be a very clear understanding of what is monetary policy and what is not monetary policy if the Fed needs to know what is bank regulation and therefore more in play for criticism versus what is monetary policy and within the Fed’s purview to do as it wishes. Federal independence will be better able to be protected and assured once we know what it is. But we don’t know what it is. What we do know is the Fed wants to pretend that it can’t be criticized for the decisions that it makes, and that’s not independence. A Federal Reserve that will not be criticized will not realize that it makes mistakes will not recognize its mistakes. It will not learn from its mistakes. It will keep making those mistakes again and again. This situation is not a good situation for monetary policy. There is a lot of work to do, and Kevin Warsh has a relatively ambitious agenda I wish him well and I hope that he remains focused on the job at hand..

END