Inflation-- does it even matter? …to the Fed

2% inflation as nostalgia?

Inflation-- does it even matter?

…to the Fed?

Nostalgia…

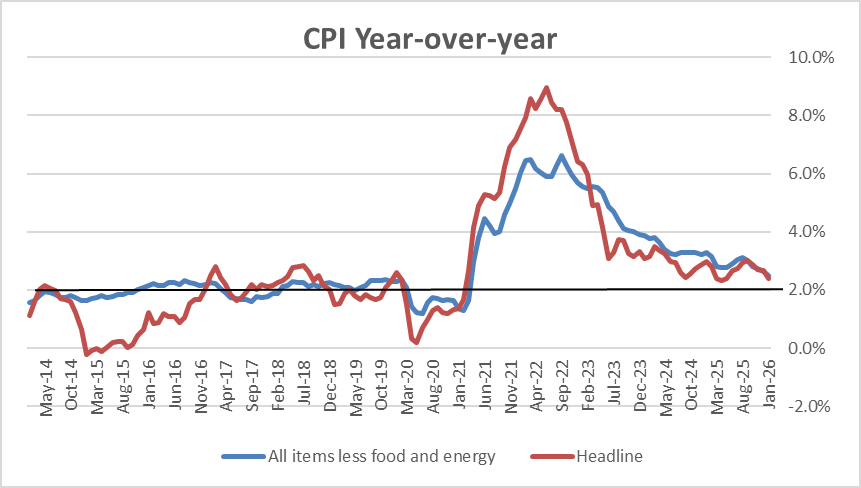

We last saw CPI inflation below 2% in March of 2021 (nostalgia!). It has been 4 3/4 years since the Fed has hit its target that is expressed formally in terms of the PCE not in terms of this CPI. But the relationship between these two price indices has become intertwined and less distinct.

I began working at the Fed (NY Fed) in 1977 and left the Fed to become a Fed watcher officially in early 1983. I’ve been watching the Fed from the outside ever since (over 40-years!) getting to know the various FOMC members, and their views, getting to see the models or the paradigms that the Fed sets to make policy.

The Fed’s view towards policy and how economics works, of course, has changed over this span…. quite a great deal. Back to the 1960s there was a framework of monetary aggregates, M1 through M5, that served as some reference for what monetary policy was doing; but it was a framework of reference that really wasn’t watched very closely.

Crossing the double yellow line *

The Fed allowed money growth to surge and inflation to slip higher - to become solidified - and to continue to accelerate in the 1970s. Of course, in the late 70s and early 80s Paul Volcker basically rode to the rescue on the back of Jimmy Carter’s demise, as the nation had had its fill of inflation so thoroughly that while there were many protests, particularly from banks in the building trades, the Fed still was able to marshal support for incredibly high interest rates to bring inflation down.

To do this, the Fed engaged in an approach called ‘monetarism’ or at least it said it did for a short period of time. Its attempt to constrain money growth to a strict set of targets caused interest rates to rise sharply and allowed the Federal Reserve to shrug its shoulders and say, well, we’re not making these interest rates it’s the overshoot of money demand relative to our supply targets. This, public charade, helped to shield the Fed from broader controversy and brought inflation to heel and eventually it was followed by a long period of price stability that we have basked in until COVID struck and a new round of inflation sprang up… in some sense out of nowhere. But, of course, inflation was from somewhere, and that somewhere was excessive fiscal spending, excessive monetary expansion, and diminished supply capabilities that occurred during COVID…nowhere indeed.

Selective remembrance…and the way we REALLY were

This episode is emblazoned in the memories of any market participant who lived through it although we are now talking about a period that’s 45 years ago and therefore there are not very many veterans from trading rooms who are still in the trenches. The Federal Reserve prefers to recall this episode as how it earned its stripes and how it could be trusted to do the right thing - no matter how painful- to bring inflation under control. However, this bit of “selective remembrance” requires that you forget that the Federal Reserve had allowed inflation to get out of control badly - out of control for a decade - before it decided that it needed to pay attention to inflation.

Does inflation matter?

OK so in asking whether inflation matters I’m looking back at this. And I’m also trying to get you to take a close look at our current situation which is nearly five years long with inflation overshooting its target. Do we have to wait another five years to make it an even decade before the Federal Reserve will get reli

gion and regain control of inflation? Is going to take a decade as in the 1970s-80s?

Focused cynicism

Yes, there is a certain cynicism here. But it’s also true that in the 1970s and ‘80’s the Federal Reserve engaged in a very special sort of denial. At that time, of course, there were special things going on in the economy. OPEC had been formed and shot oil prices up sharply in the early 1970s and there were several oil shocks that followed. In 1971 the Bretton Woods system of exchange rates collapsed, and we wound up with a fluctuating exchange rate system that turned out to be a wonderful breeding ground for allowing and spreading inflation. On balance Federal Reserve policy was too focused on the unemployment rate and on trying to stabilize it and shield the economy - the real sector, total employment - from real world conditions that were occurring. But, the Fed had no reason to think those conditions would be temporary or that could be solved by running a higher inflation rate. Higher begat higher still…

When inflation accelerates above the past level of interest rates…

In fact, had the Fed thought about it, it should have come to a very different decision about the way it conducted policy. One of the most perplexing things in hindsight is to realize that we had a banking system with savings and loan institutions faced with interest rate ceilings and that the inflation rate was bumping up against the interest rate ceiling that these banks were able to pay. Certainly, someone at the Fed should have seen what this meant for these institutions and LONG BEFORE WE GOT THERE… as well as what it would mean for them prospectively, if inflation was allowed to rise even higher.

It meant that these financial institutions that had spent their entire institutional lives acquiring financial assets with yields at levels that assumed there would be interest rate ceilings in place to deliver a profit. But now, the government was faced with an inflation so high it was going to have to raise interest rates above these ceilings.

The business cycle model

This had happened in the past… And when this had happened in the old business cycle model, something happened that we call ‘disintermediation.’ This means that, as rates went up above the interest rate ceilings, S&L’s could not raise money and so they would not be able to on-lend for mortgages to the housing market. The sector would basically collapse and this would help weaken the economy, run a recession, and that would cure inflation. A somewhat painful process but a contained paradigm.

Structurally rising inflation is not a business cycle model

But this business cycle model did not fit with the structural inflation situation that had evolved. A situation where inflation would run above the interest rate ceilings and continue to accelerate… this in fact was the S&L crisis model or the bankruptcy model for the sector. This is what the Fed headed for and this is what happened. Eventually reality required that interest rate ceilings were removed and with their removal interest rates went up a great deal which they had to address higher inflation and the collateral damage was that the savings and loan industry was decimated.

So why reference the S&L Industry now?

The Fed has actually done a very good job of replicating the exact same mistake that it made in the late 70s and the early 1980s. Like many historic comparisons the comparison here is not perfect but the analogy actually fits very well. The difference is that in the 1970s inflation had gone wild and created a long lived problem for policy tha became worst as inflation rose relative to an existing regulation, an interest rate ceiling. There was no such snafu before COVID. However, there had been a ‘similar’ situation in which inflation had been extremely steady <and low> for an extremely long time so that interest rates we’re actually running below the rate of inflation. Although inflation was low (and stable!) interest rates were even lower. The comparison with the S&L crisis comes when COVID strikes and the Federal Reserve goes into denial about inflation being real. The Fed tries to argue that because it kept inflation low it can take its time and bring inflation back to heel slowly. This is a mistake. It basically lays the groundwork for the same classic mistake that the Fed made during the S&L problem. The main difference that may make the comparison seem jarring to you, is that, then, inflation was high, and then, it accelerated, while in this instance, inflation is low, but then it accelerates. But the real event that drives this to make it a crisis situation is that inflation and interest rates we’re at a certain level and very stable for a long period and then, all of a sudden, the level of inflation jumps higher than what it was previously and this causes all of the assets that are on the books of financial institutions to move instantly to a situation where they are underwater. They are discounted. They are showing losses on a mark-to-market basis. The is an immediate loss of capital by market participants – just as in the S&L crisis.

The vehicle that financial institutions have (now) that they did not have in the S&L crisis was the ability to use hold-to-maturity (HTM) pricing to sweep these capital losses off their balance sheet but into a footnote where they’d be collected and eventually reported. And whether they’re reported or not does not make a difference, if a bank has to be liquidated. If a bank has to be liquidated it will have to liquidate its securities at market prices not at some imagined book value pricing.

When Powell made them howl

The Fed in 2000 worsen this situation by encouraging people to think inflation would be moderate and temporary. We are 4 ¾ years later and still over target on inflation. At one point, Chair Powell vowed to keep rates low as Bernanke had after the Great Recession. But inflation did not cooperate so Powell’s promise became a trap for anyone who listened to him and believed him. Moreover the Fed pumped up the money supply increasing banking system liabilities and forcing banks to absorb assets at what would prove to me multi-year yield lows. Not exactly like req-Q interest rate ceiling but then not so different either...in their own way

Deja Vu-Doo?

My argument here is simple, that the Federal Reserve was making the exact same mistake in 2026 that it had made-up until 1980 by ignoring inflation that had run hot. Even when faced with the risk of tariffs the Federal Reserve was not motivated to take steps to control inflation but rather to continue to cut rates steadily, even when the inflation rate remained above target and remained steady. Having inflation not accelerate was enough for the Fed to cut rates even though not accelerating inflation was still higher than the target it had promised, and, of course, what makes 2026 different from the late ‘70s and ‘80s is that in the earlier period there was no inflation target although we didn’t need an inflation target to know that inflation was way out of control and out of hand.

The Covid illusion

And what we subsequently saw with COVID is that while the unemployment rate went up very sharply in the government-created recession (…that occurred when people were told to stay home and not go to work), but we also saw the unemployment rate come down very quickly when there was recovery. We have every reason to think that, had the Fed followed up the COVID, downturn with a more aggressive anti-inflation policy, it could have controlled inflation better, even if the economy had slipped into a classical business cycle downturn of some sort induced by higher interest rates. Then, there would have been a recovery from it. The job market would have recovered fully and completely and probably quickly. Inflation could have been brought down to target and set the stage for a more sustainable recovery.

But like the dog that didn’t bark, this is the policy that wasn’t chosen. And the dog that didn’t bark told you something about what was really going on. And the policy that wasn’t chosen also tells us something about what’s really going on about where the Fed really places its values and also allows us to look a little bit more clearly into the future if we’re going to be honest about it. The Fed does not care about moderate inflation. But then that is how out-of-control inflation starts…

…a long freebee but it ends here…